Statements of banks contain any records on the impact of IFRS 15. IFRS 15 Revenue Recognition. As a result of. Under IFRS 15 the bank accounts for consideration payable to a customer such as a cashback award as a reduction of the transaction price and therefore of revenue unless the payment to the customer is in exchange for a distinct good or service that the customer transfers to the bank. To help you drive your implementation project to the finish line weve pulled together a list of key considerations that many banks need to focus on. IFRS 15 may change the way some banks account for their contracts. Financial instruments and other contractual rights or obligations within the scope of IFRS 9 Financial Instruments IFRS 10 Consolidated Financial Statements IFRS 11 Joint Arrangements IAS 27 Separate Financial Statements and IAS 28 Investments in. Download pdf 2508 KB. It applies to the majority of contracts with customers where a business has. Entities are required to describe the nature and effect of initially applying the new standards.

From January 1st 2018 a new Accounting Standard becomes mandatory for reporting the Revenue Recognition in Contracts with Clients IFRS 15 becomes effective.

Customer Loyalty Programmes and Other Options for Additional Goods or Services IFRS 15 Last updated. The IASBs Standard IFRS 15 Revenue from Contracts with Customersis now effective for periods beginning on or after 1 January 2018 with earlier adoption permitted. This is not merely a financial reporting issue. As complex multi-national institutions it is important for banks to be alert at all times to accounting changes. Under IFRS 15 the bank accounts for consideration payable to a customer such as a cashback award as a reduction of the transaction price and therefore of revenue unless the payment to the customer is in exchange for a distinct good or service that the customer transfers to the bank. The impact of IFRS 15 will vary depending on the precise nature of a banks business.

Applying these new rules may result in changes to the profile of revenue and in some cases cost recognition. As complex multi-national institutions it is important for banks to be alert at all times to accounting changes. Beyond IFRS 9 Financial Instruments there are many other aspects of financial reporting that impact this sector including global benchmark reform and the effects of the COVID-19 coronavirus pandemic. Leases within the scope of IAS 17 Leases. IFRS 15 replaces IAS 11 IAS 18 IFRIC 13 IFRIC 15 IFRIC 18 and SIC31. Financial instruments and other contractual rights or obligations within the scope of IFRS 9 Financial Instruments IFRS 10 Consolidated Financial Statements IFRS 11 Joint Arrangements IAS 27 Separate Financial Statements and IAS 28 Investments in. The Standard is the result of a joint project of IASB and FASB to develop a converged set of accounting principles for revenue recognition. 1 Identify the contract with the customer. IFRS 15 for Banks with SAP Revenue Accounting. Disclosure of the nature and effect of changes in accounting policies.

The impact of IFRS 15 will vary depending on the precise nature of a banks business. In September 2015 the Board issued Effective Date of IFRS 15 which deferred the mandatory effective date of IFRS 15 to 1. Some industries will experience greater changes than others. IFRS 15 may change the way some banks account for their contracts. 1 Identify the contract with the customer. Recognition policies and practices IFRS 15 is more prescriptive in many areas relevant to the banking and securities sector. To help you drive your implementation project to the finish line weve pulled together a list of key considerations that many banks need to focus on. These analyses are within the mainstream of studying how complete and prospective is the information contained in the financial statements for external users. The Standard is the result of a joint project of IASB and FASB to develop a converged set of accounting principles for revenue recognition. IFRS 15 Revenue Recognition.

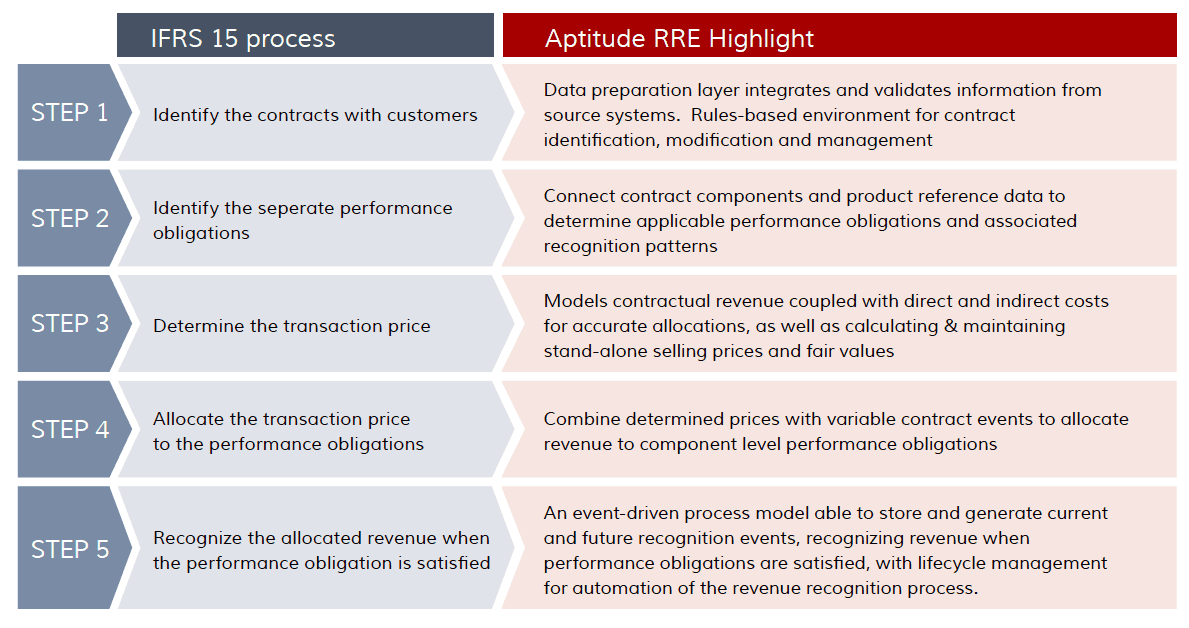

IFRS 15 Revenue from Contracts with Customers applies to all contracts with customers except for. Entities are required to describe the nature and effect of initially applying the new standards. Some industries will experience greater changes than others. IFRS 15 enhances the process of Revenue Recognition by establishing a 5 steps process. As a result of. To help you drive your implementation project to the finish line weve pulled together a list of key considerations that many banks need to focus on. Disclosure of the nature and effect of changes in accounting policies. IFRS 15 may change the way some banks account for their contracts. IFRS 15 replaces IAS 11 IAS 18 IFRIC 13 IFRIC 15 IFRIC 18 and SIC31. The IASBs Standard IFRS 15 Revenue from Contracts with Customersis now effective for periods beginning on or after 1 January 2018 with earlier adoption permitted.

To help you drive your implementation project to the finish line weve pulled together a list of key considerations that many banks need to focus on. Customer Loyalty Programmes and Other Options for Additional Goods or Services IFRS 15 Last updated. The IASBs Standard IFRS 15 Revenue from Contracts with Customersis now effective for periods beginning on or after 1 January 2018 with earlier adoption permitted. It is imperative that entities take time to consider the impact of the new Standard. As complex multi-national institutions it is important for banks to be alert at all times to accounting changes. Applying these new rules may result in changes to the profile of revenue and in some cases cost recognition. Statements of banks contain any records on the impact of IFRS 15. This is not merely a financial reporting issue. IFRS 15 Revenue from Contracts with Customers applies to all contracts with customers except for. Disclosure of the nature and effect of changes in accounting policies.

As complex multi-national institutions it is important for banks to be alert at all times to accounting changes. This is not merely a financial reporting issue. Entities are required to describe the nature and effect of initially applying the new standards. IFRS 15 provides a comprehensive framework for recognising revenue from contracts with customers. Disclosure of the nature and effect of changes in accounting policies. From January 1st 2018 a new Accounting Standard becomes mandatory for reporting the Revenue Recognition in Contracts with Clients IFRS 15 becomes effective. It applies to the majority of contracts with customers where a business has. IFRS 15 Revenue from Contracts with Customers applies to all contracts with customers except for. Customer Loyalty Programmes and Other Options for Additional Goods or Services IFRS 15 Last updated. The Standard is the result of a joint project of IASB and FASB to develop a converged set of accounting principles for revenue recognition.