Fabulous Bad Debts In Cash Flow Statement Balance Sheet Of A Company

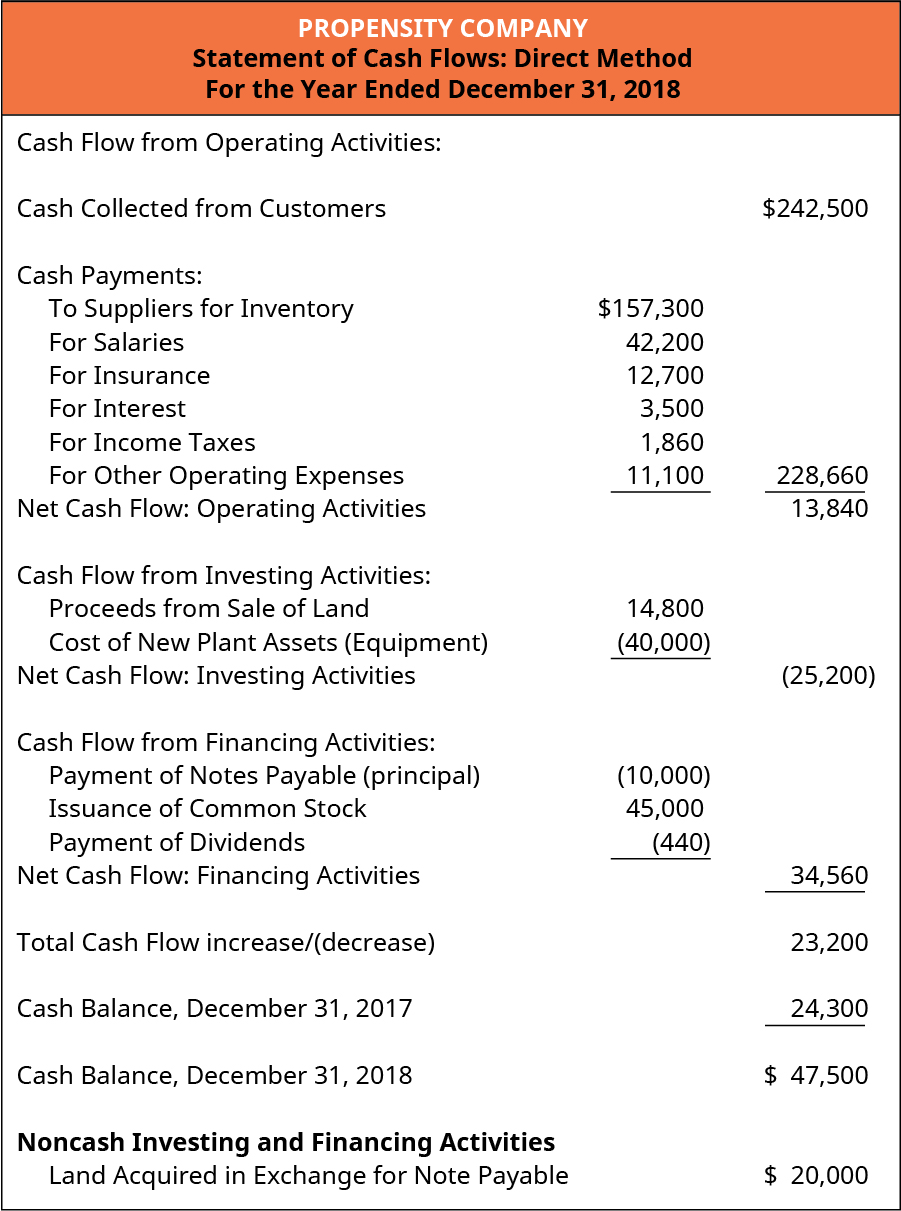

Appendix Prepare A Completed Statement Of Cash Flows Using The Direct Method Principles Of Accounting Volume 1 Financial Accounting

First lets determine what the term bad debt means. Financing is the source of the cash that we will be using to invest in non-current assets. Definition of Bad Debts Expense Bad debts expense is related to a companys current asset accounts receivable. Net cash flow or the total resultant change in cash and cash equivalents is calculated using either the direct or indirect method. Determination of Net change on Cash and Cash Equivalents. Bad debts expense results because a company delivered goods or services on credit and the customer did not pay the amount owed. Accounts receivable can be one the largest assets on the balance sheet depending on the company and industry. We also include cash outflows in this section that relate to. That gives you a more realistic picture of your businesss income than assuming every receivable will be paid in full. Thus financing activities mainly involves cash inflows for a business.

Its worth noting that cash flow statements can be affected by non-cash transactions like depreciation or bad-debt expenses.

What is Bad Debt. Financing can come from the owner owners equity or from liabilities loans. Additionally many businesses choose to add supplemental information about large transactions that dont involve cash like converting debt to equity or issuing shares in return for assets. As per AS-3 Revised the objective of cash flow statement is to provide information about cash flows of an enterprise which is useful in providing the users of financial statements with a basis to assess the ability of an enterprise to generate cash and cash equivalents to utilize those cash flows. Indirect Impact of Bad Debt If your company prefers to use a bad debt reserve which is an amount set aside to cover bad receivables then the impact on the cash flow statement. Elimination of non cash expenses eg.

If a companys business operations can generate positive cash flow negative overall cash flow isnt necessarily. That gives you a more realistic picture of your businesss income than assuming every receivable will be paid in full. Bad debts expense results because a company delivered goods or services on credit and the customer did not pay the amount owed. Debited in PL AC is to be added back as non cash item and the changes in the Balance of the Prov. AC as per the Balance sheet is to be added or subtracted accordingly as Changes in Working capital. Can you explain me the treatment of Provision for Bad debts in Cash flow statement under indirect method. Sometimes at the end of the fiscal period Fiscal Year FY A fiscal year FY is a 12-month or 52-week period of time used by governments and businesses for accounting purposes to formulate annual when a company goes to prepare its financial statements Three Financial Statements The three financial statements are the. If you really want to argue yes it shows up in the income statement but somewhere along the cash flow statement would need to add it back to cancel it out as it is a non-cash activities to ensure the amount does not affect the cash flow statement. The cash flow statement looks at the inflow and outflow of cash within a company. A cash flow statement discloses net increase or decrease in cash during an accounting period.

AC as per the Balance sheet is to be added or subtracted accordingly as Changes in Working capital. Removal of expenses to be classified elsewhere in the cash flow statement eg. Like Alternative A the bad debts provision is viewed implicitly as a revenue deduction rather than a noncash expense and the reconciliation does not include a separate line item for the bad debts provision. Financing can come from the owner owners equity or from liabilities loans. Financing is the source of the cash that we will be using to invest in non-current assets. Depreciation amortization impairment losses bad debts written off etc. It should be noted that bad debts do however form part of the calculation of cash generated from operations when using the indirect cash flow statement which is the preferred method in the US. The bad debt provision reduces your accounts receivable to allow for customers who dont pay up. Definition of Bad Debts Expense Bad debts expense is related to a companys current asset accounts receivable. First lets determine what the term bad debt means.

Reconciliation of Operating Profit to Net Cash Flow from Operating ActivitiesCash flow is derived from the operating activities of the businessfirm and Operating profit isadjusted for changes in. Download the Question Worksheet. Financing is the source of the cash that we will be using to invest in non-current assets. In other words the sale. Uncollectible Accounts and the Cash Flow Statement. A cash flow statement discloses net increase or decrease in cash during an accounting period. After the determination of cash flows from the operating activities investing activities and financing activities their results are calculated and added to ascertain the net change in cash and cash equivalents. First lets determine what the term bad debt means. This type of reconciliation is occasionally found in. Bad debt expense from a write off is subtracted from Sales Revenues lowering Total Sources of Cash.

My assumption is that the prov. The cash flow statement looks at the inflow and outflow of cash within a company. It is the final step in the preparation of cash flow statement. Uncollectible accounts being written off as bad debt expense have no impact on cash flow statements except in the most indirect manner. Statement of Retained Earnings. Determination of Net change on Cash and Cash Equivalents. Net cash flow or the total resultant change in cash and cash equivalents is calculated using either the direct or indirect method. Writing off bad debt is a non-cash event and therefore not placed on cash flow statement. Elimination of non cash income eg. Elimination of non cash expenses eg.

In other words the sale. If you really want to argue yes it shows up in the income statement but somewhere along the cash flow statement would need to add it back to cancel it out as it is a non-cash activities to ensure the amount does not affect the cash flow statement. It is where we get cash from. We also include cash outflows in this section that relate to. Uncollectible accounts being written off as bad debt expense have no impact on cash flow statements except in the most indirect manner. Thus financing activities mainly involves cash inflows for a business. My assumption is that the prov. Determination of Net change on Cash and Cash Equivalents. Accounts receivable can be one the largest assets on the balance sheet depending on the company and industry. Statement of Retained Earnings.