Impressive Accounting For Increase In Ownership Of Subsidiaries Air India Financial Statements

Investments Requiring Consolidation Principlesofaccounting Com

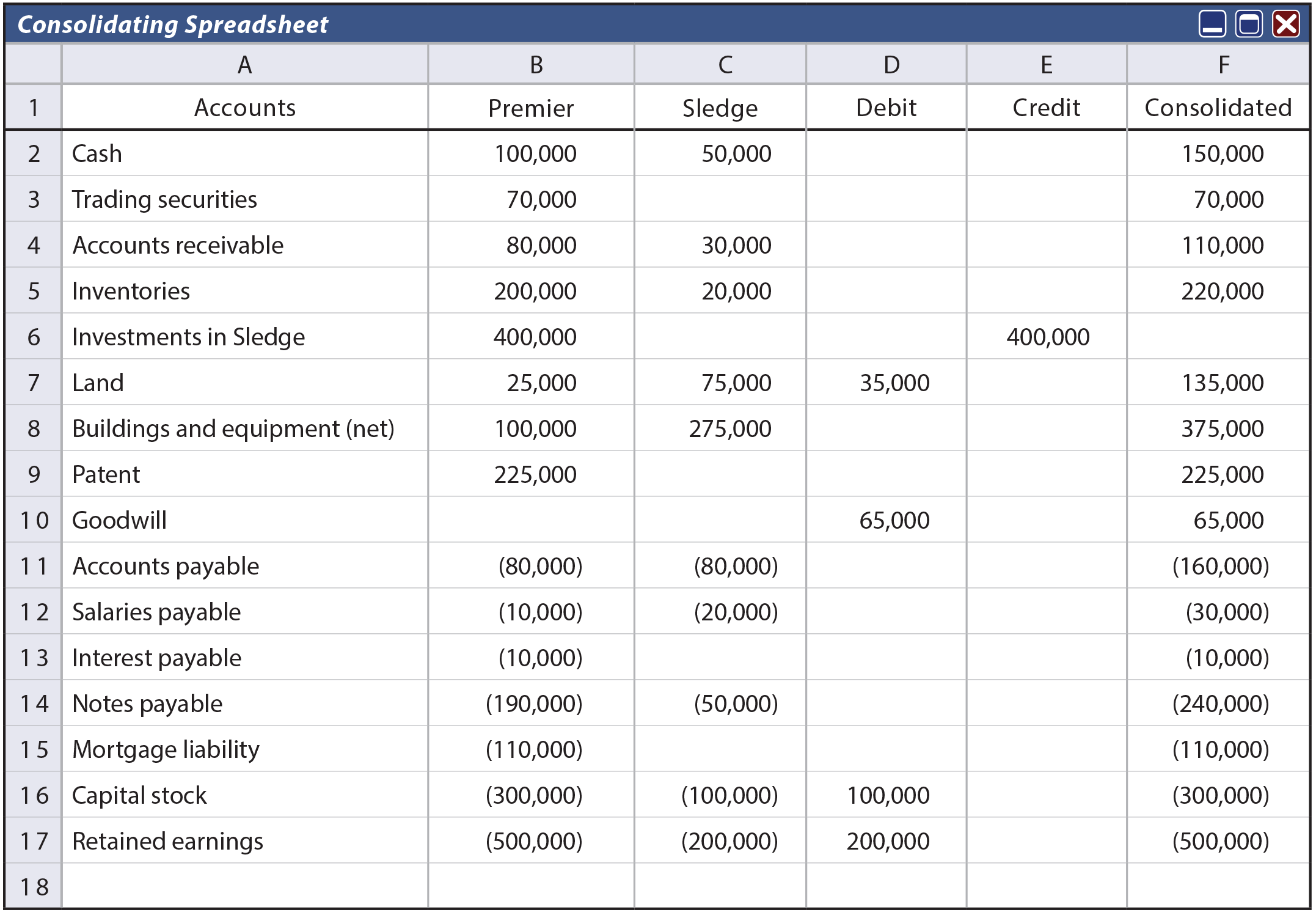

Accounting for subsequent activities Changes in the amount of investment of the subsidiary such as the parent purchasing additional shares of ownership or divesting some of their ownership are accounted for by adjusting the investment asset. As per IFRS 10 Consolidated Financial Statements a parent entity is required to prepare consolidated financial statements that comply with IFRS. The parents ownership interest increases or decreases without loss of control. Accountants use either the cost method the equity method or the consolidation method to account for businesses investing in other businesses. The accounting depends on whether control is retained or lost. Accounting for Increase in Ownership of Subsidiary. This blog post aims to provide an insight into the accounting treatment for Subsidiaries and Associates which is definitely a crucial area in F1 and can be highly applicable to Thomas Fines Tea TFT. Partial disposal of an investment in a subsidiary while control is retained. The parent company can. The resulting excess of subsidiary fair value over book value is assigned to franchises and amortized at the rate of 10000 per year.

56 Change in Level of Ownership or Degree of Influence 140 561 Increase in Level of Ownership or Degree of Influence Control Initially Obtained Equity Method to Consolidation 141 562 Increase in Level of Ownership or Degree of Influence Significant Influence.

The parents ownership interest increases or decreases without loss of control. A subsidiary is a company that is controlled by its parent company. Business combinations with no transfer of consideration 107 131 Accounting requirement and examples 107 132 Combinations by contract alone 107 1321 Example of a dual listed structure 107 1322 Accounting for a combination by contract 108. There is a non-controlling interest in the subsidiary. The resulting excess of subsidiary fair value over book value is assigned to franchises and amortized at the rate of 10000 per year. The accounting depends on whether control is retained or lost.

This is accounted for as an equity transaction with owners and gain or loss is not recognised. Accounting for subsequent activities Changes in the amount of investment of the subsidiary such as the parent purchasing additional shares of ownership or divesting some of their ownership are accounted for by adjusting the investment asset. Partial disposal of an investment in a subsidiary while control is retained. Accounting for Increase in Ownership of Subsidiary. FRS 2 Accounting for subsidiary undertakings FRS 102 T he identifiable assets and liabilities of that subsidiary undertaking should be revalued to fair value and goodwill arising on the increase in interest should be calculated by reference to those fair values. This blog post aims to provide an insight into the accounting treatment for Subsidiaries and Associates which is definitely a crucial area in F1 and can be highly applicable to Thomas Fines Tea TFT. The subsidiary acts and operates as its own entity but it is still connected to the larger company. The parents ownership interest increases or decreases without loss of control. The parent company can. A subsidiary is a company that is controlled by its parent company.

Accountants use either the cost method the equity method or the consolidation method to account for businesses investing in other businesses. FRS 2 Accounting for subsidiary undertakings FRS 102 T he identifiable assets and liabilities of that subsidiary undertaking should be revalued to fair value and goodwill arising on the increase in interest should be calculated by reference to those fair values. As per IFRS 10 Consolidated Financial Statements a parent entity is required to prepare consolidated financial statements that comply with IFRS. This equity treatment for the gain is consistent with the economic unit notion that as long as control is maintained payments received from owners of the firm are considered contributions of capital. There is a non-controlling interest in the subsidiary. The accounting depends on whether control is retained or lost. For example if the parent bought 50000 worth of a subsidiarys stock it would debit Intercorporate Investment for 50000 to reflect the new asset and credit cash for 50000 to reflect the cash outflow. Partial disposal of an investment in a subsidiary while control is retained. 126 Accounting in the investing entity where separate financial statements are prepared 106 13. This blog post aims to provide an insight into the accounting treatment for Subsidiaries and Associates which is definitely a crucial area in F1 and can be highly applicable to Thomas Fines Tea TFT.

The parent company can. The subsidiary acts and operates as its own entity but it is still connected to the larger company. There is a non-controlling interest in the subsidiary. The resulting excess of subsidiary fair value over book value is assigned to franchises and amortized at the rate of 10000 per year. Accountants use either the cost method the equity method or the consolidation method to account for businesses investing in other businesses. As per IFRS 10 Consolidated Financial Statements a parent entity is required to prepare consolidated financial statements that comply with IFRS. The parents ownership interest increases or decreases without loss of control. Accounting for subsequent activities Changes in the amount of investment of the subsidiary such as the parent purchasing additional shares of ownership or divesting some of their ownership are accounted for by adjusting the investment asset. Following the acquisition Middles book value rises to 1080000 by the end of 2011 denoting a 380000 increment during this three-year period 1080000 700000. This blog post aims to provide an insight into the accounting treatment for Subsidiaries and Associates which is definitely a crucial area in F1 and can be highly applicable to Thomas Fines Tea TFT.

Or the parent loses control of the subsidiary. The NCIs value changes due to the subsidiarys profits and losses. Business combinations with no transfer of consideration 107 131 Accounting requirement and examples 107 132 Combinations by contract alone 107 1321 Example of a dual listed structure 107 1322 Accounting for a combination by contract 108. As per IFRS 10 Consolidated Financial Statements a parent entity is required to prepare consolidated financial statements that comply with IFRS. For example if the parent bought 50000 worth of a subsidiarys stock it would debit Intercorporate Investment for 50000 to reflect the new asset and credit cash for 50000 to reflect the cash outflow. The 15000 gain on sale of the subsidiary shares is not recognized in income but is reported as an increase in owners equity. This equity treatment for the gain is consistent with the economic unit notion that as long as control is maintained payments received from owners of the firm are considered contributions of capital. Accountants use either the cost method the equity method or the consolidation method to account for businesses investing in other businesses. The resulting excess of subsidiary fair value over book value is assigned to franchises and amortized at the rate of 10000 per year. The parent company can.

The parent company can. This is accounted for as an equity transaction with owners and gain or loss is not recognised. The subsidiary acts and operates as its own entity but it is still connected to the larger company. A subsidiary is a company that is controlled by its parent company. This blog post aims to provide an insight into the accounting treatment for Subsidiaries and Associates which is definitely a crucial area in F1 and can be highly applicable to Thomas Fines Tea TFT. The 15000 gain on sale of the subsidiary shares is not recognized in income but is reported as an increase in owners equity. The NCIs value changes due to the subsidiarys profits and losses. Partial disposal of an investment in a subsidiary while control is retained. Accountants use either the cost method the equity method or the consolidation method to account for businesses investing in other businesses. FRS 2 Accounting for subsidiary undertakings FRS 102 T he identifiable assets and liabilities of that subsidiary undertaking should be revalued to fair value and goodwill arising on the increase in interest should be calculated by reference to those fair values.